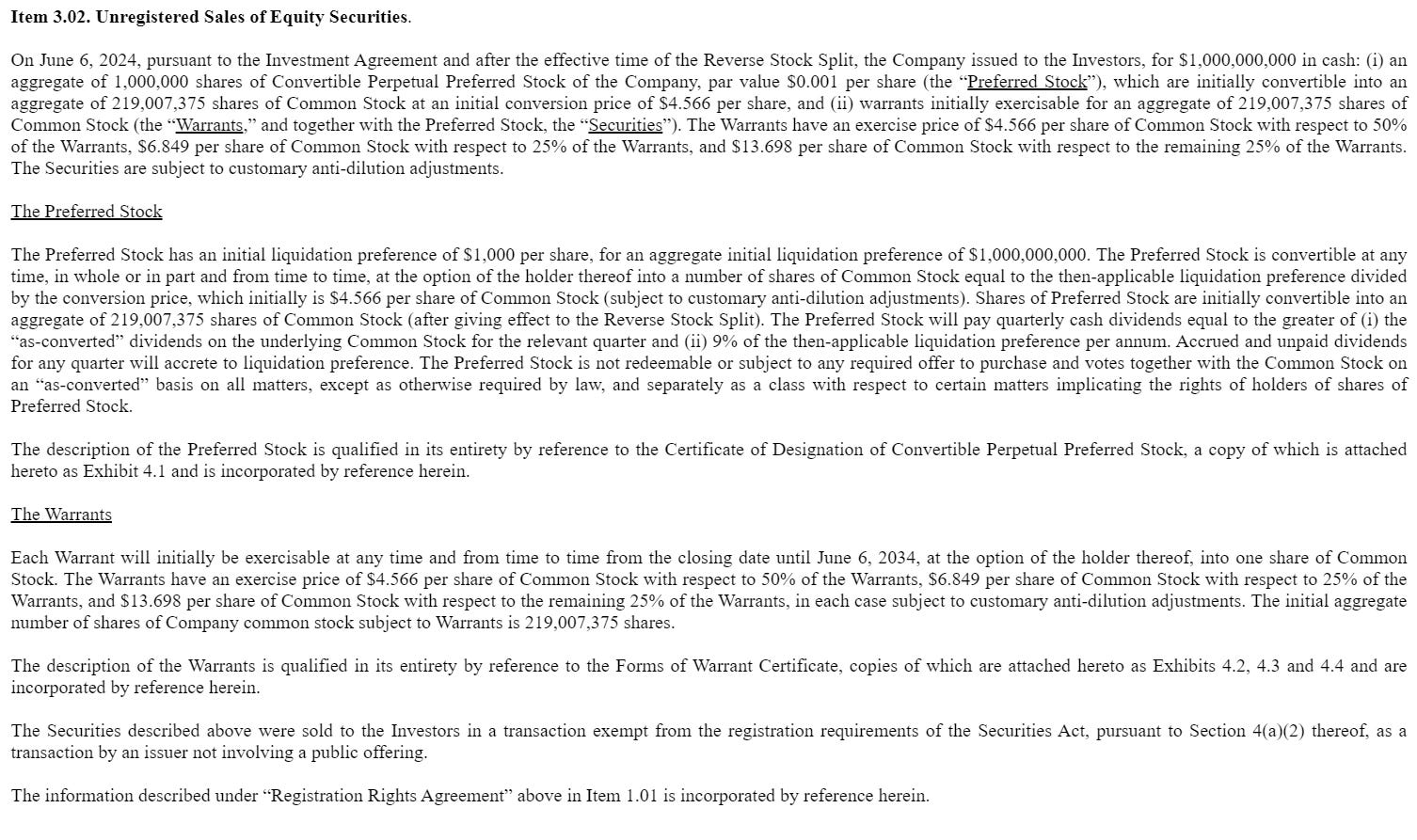

7. QXO: With All Due Respect...

Like many other market participants I have a lot of respect for Brad Jacobs. He’s the kind of operator who is worth following and co-investing with - at the *right* valuation. A few years ago, I lucked into a no-brainer long, high-IRR % opportunity in XPO in A/H trading when Spruce Point posted a short report on it that had some simple inaccuracies. That took just 2 hours of work for me. Brad Jacobs - being the exceptional principal that he is - took appropriate action through big share buybacks. Both the long-term XPO holders and short-term renters (like myself) benefited. So I have kept loose track of Jacobs’s recent moves, which brings us to QXO.

QXO I think offers me a similar no-brainer opportunity for monetary gain, but this time on the short side. Shorting securities associated with folks I really respect needs to clear an even higher-than-normal bar, and I think QXO does that.

QXO is effectively an unusually large market-cap cash shell with a small IT services business (SWK Tech) attached to it. Revenues are on a c.$50M annual run-rate and FCF is close to 0. Prior to last night’s private placement, QXO had $1B of net cash and it was fiendishly confusing to figure out what was the actual sharecount and thus market cap & EV. To wit, see the extract from the 8-K that was filed a week ago:

Basically, my best read of that 8-K is that before yesterday night, for all intents and purposes the ‘real’ sharecount was north of 400M. Share price before yesterday was around $200 per share. Thus you get a market cap north of $80B and similar EV (given relatively insignificant net cash). The EV/FCF multiple was infinite; EV/sales was higher than 1,500x. So I shorted some shares in the $180-200 range, but it seems, I didn’t short enough. The borrow rate of 20% is not pleasant but I did it anyway.

Now let’s look at last night’s private placement news:

So there you have it. The company is selling securities at prices way below $200 and sharecount is increasing further. Pre-market, QXO is trading at $112 per share as of this writing. You can do the maths - the valuation is still pretty disconnected from the actual scale of the business. Shorting QXO still seems like a relative no-brainer.

Given the track record of the people at the helm, I would not be surprised if they create billions of $ of value like they have several times before. But the starting valuation for the outside investor here is unfavorable and for now, I am aligned with the company and its principals. They are selling securities, and therefore, so am I. I am willing to flip and be net long because of who is running things, but not at the prevailing market price.

DISCLAIMER: Nothing here constitutes a buy/sell recommendation on any security and the reader is encouraged to always exercise diligence and do their own work. I can be long/short securities that are mentioned here and this can change without warning. Shorting usually is a terrible idea and careful sizing / monitoring is imperative.

Well done. Either my stock charts are off due to wonky share counts or this was an absolutely incredible short call. Either way you got a sub from me.

what price would you buy shares long?