2: On 'quality' investing and price-to-book ratios

‘Quality’ investing is all the rage nowadays. The investing community (including yours truly) seems to have ‘rediscovered’ and latched on to it as if it is a new concept or some sort of a long lost art form. Below are some of the recently published books advocating for ‘quality investing’.

But the idea of ‘quality’ investing is not new. Buffett has been talking about the importance of business quality since at least the late 90s; to wit, see the quote below.

“But time is the friend of the wonderful business; it is the enemy of the lousy business. If you are in a lousy business for a long time, you will get a lousy result even if you buy it cheap. If you are in a wonderful business for a long time, even if you pay a little bit too much going in you will get a wonderful result if you stay in a long time. “ - Buffett, 1998.

It’s a completely reasonable idea - some businesses can grow or preserve revenue and operating cash flows without requiring too much incremental cash-outs along the way, and when this situation persists over long periods of time, the results to the equityholder can be rather favorable.

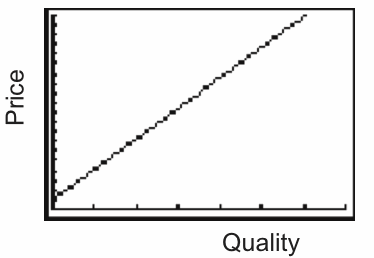

But there are many challenges with ‘quality’ investing. First, what is the ‘right’ price to pay for a superior business? What is the shape of the relationship between price and business quality? When people try to illustrate it via a diagram or graph, usually they go for the linear shape (see below).

It is tempting to think of the relationship as linear. A linear chart also neatly fits the idea that “there is a right price for everything” and that every horse in a horse-race can be effectively handicapped. But if we go back and think about Buffett’s quote, clearly the relationship between business quality and price should be more exponential or ‘cubic’ in nature. There are certain setups for which an extremely low price should be demanded. An extreme example is when someone buys equity control in a failed business with tons of debt claims ahead of it for just 1 dollar. Less extreme but sensible examples are businesses with very bad principal-agent setups. Imagine a deeply untrustworthy and/or incompetent management team that is wasting cash or treating the business as their personal piggybank, with no realistic prospect of shareholder (or activist) pressure due to dual-class share structure or outsized family control. A P/E of 8x might not be cheap enough for something like that. And even in cases where management is relatively honest and corporate governance is such that the board would actually seriously consider shareholder proposals, a statistically cheap price (say a P/E of 8x and a dividend yield of 8%) may not be cheap enough for an appropriate risk-adjusted return. There can be many reasons for this. The dividend might not be covered by available FCF. The business’s profits and FCF might be more likely to shrink than to grow due to a commoditized industry with low barriers to entry and price-taking. And if we dispense with ‘flow’-based valuation metrics like earnings, FCF and EBITDA and move towards ‘stock’-based metrics like multiples of book value (P/BV, P/TBVPS) or invested capital (EV/IC), relying on these as an indicator of cheapness is dumb *unless* the business is actually liquidating or unless there is a significant chance that there are motivated strategic / financial buyers for the entire business. Imagine I incorporate a new business tomorrow and fund it with $1000. I then promptly spend that $1000 of cash on 2 Yeti coolers costing $500 each, and I then bury them in my backyard. I now have a business with $1000 of tangible assets (the 2 Yeti coolers) and no liabilities, i.e. $1000 of tangible equity. Well guess what. My ‘business’ is not actually worth $1000 now. Same thing if I spend $100 million constructing an amusement park on a remote uninhabited island. Stranded, second-hand and useless assets that nobody else really wants aren’t worth what they were bought for. And, when you hold shares in a business that looks cheap vs the assets recorded on the balance sheet and are rooting for monetization, you are betting against management’s powerful human instinct that drives them towards their own survival. They want to perpetuate their paychecks. In 99.9% of cases, management’s incentive is to keep the lights on and keep the business running, not liquidate assets and dividend the money out to you, the shareholder. Management wants to preserve status quo. The CEO is usually powerfully incented to see things in a positive light and will then do his/her best to try to convince the shareholders of the same, i.e. that it is a good idea to take that operating free cash flow and invest it into new plants or to buy up smaller competitors - even if the industry is still fundamentally a crappy one. Trying to grow the business in a bad industry aligns with the management’s self-interest - CEOs of larger companies (with greater revenue or more employees) get paid more. *No one* wants to liquidate themselves out of a job. And if the shareholder simply chooses to play the waiting game and wait for somebody else who values the business more highly to come along and take our business private, then good luck. It’s a dangerous game. It’s dangerous because there is the opportunity cost of potentially compounding intrinsic value through better setups. And it’s dangerous because bad management teams tend to do dumb things, and commoditized industries with intense competition and low barriers to entry are adept at creating more bad news (even when you think things just can’t get any worse). And this is where I think the more classical camp of statistical value investors fall down. They don’t demand a sufficiently low price for disadvantageous setups.

But back to ‘quality’. It’s challenging to measure business quality. Even if we try to use an ordinal system and rank businesses by quality, it’s super difficult. And boiling quality down to a single numerical indicator so that we can confidently claim something like “the business quality of Moody’s is 2x that of Coca-Cola” is impossible (I think). Because of this, I strongly emphathize with the more classic breed of value investors who are strongly allergic to paying up statistically high multiples for businesses. In my view, a good way to bridge the divide between the ‘value’ and ‘quality’ camps is to be explicit about the underlying long-term assumptions on the business, industry, and management priorities.